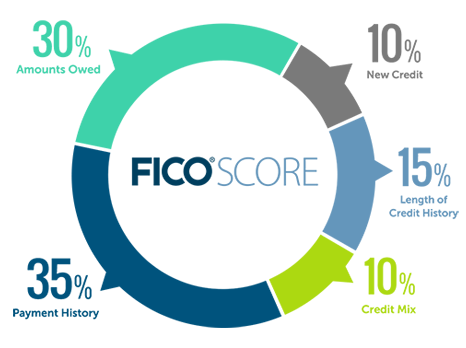

1. Payment History: The most significant component of your FICO score, accounting for about 35%, is your payment history. This section details how well you’ve managed your debts in the past. It tracks whether you’ve paid your bills on time, any missed payments and the severity of any delinquencies. Consistent on-time payments contribute positively to your score, while late or missed payments can significantly detract from it.

2. Credit Utilization: Approximately 30% of your FICO score is influenced by your credit utilization rate. This measures the proportion of your available credit that you’re currently using. High utilization, close to or exceeding your credit limits, may indicate financial stress and negatively impact your score. Aim to keep your utilization below 30% to maintain a healthy rating.

3. Length of Credit History: The length of your credit history constitutes around 15% of your FICO score. Lenders appreciate a longer credit history, as it provides a more comprehensive view of your financial behavior. This includes the age of your oldest account, the average age of all your accounts and the age of your newest account.

4. Types of Credit Used: Diversity in the types of credit you manage accounts for about 10% of your score. Creditors prefer to see a mix of credit types, such as credit cards, installment loans, and mortgages, as it demonstrates your ability to handle various financial responsibilities.

5. New Credit Accounts: Opening new credit accounts and recent credit inquiries make up roughly 10% of your FICO score. Each time you apply for new credit, a hard inquiry appears on your report. While one inquiry may have a minimal effect, numerous inquiries within a short timeframe can raise red flags for potential lenders. Inquires typically fall of a credit report after two years.

Your FICO score is dynamic and can change over time based on your financial behaviors. By understanding its components, you gain valuable insight into the factors that influence your creditworthiness. This knowledge empowers you to take deliberate steps to improve and maintain a favorable FICO score, setting the stage for your future homebuying success.

BONUS TIP:

I have found great success with having at least 4 active accounts reporting on your credit report. Two of those active accounts should be revolving accounts. Revolving credit is a line of credit that remains open even as you make payments. A secured credit card or unsecured credit card, home equity lines of credit and personal lines of credit are examples of revolving accounts. The other two accounts should be installment accounts. Of those two installment accounts, one should be a short term installment account (under 36 months) and the other should be a long term installment account (more than 36 months). An installment account allows you to borrow a lump sum of money and pay the monies back in installments. Examples of installment loans include mortgages, auto loans, student loans and personal loans.

Disclaimer:

The financial information provided here is for general informational purposes only. It is not intended as professional financial advice, and you should not rely on it as such. Always consult with a qualified financial advisor, accountant, or legal expert before making any financial decisions or taking any actions that may affect your financial well-being.